(BEING CONTINUED FROM 1/08/12)

idea that the worldwide deflation of the early 1930s was the result of a monetary

contraction transmitted through the international gold standard. But this

1929-38 and for the five countries for which data are available as our table

2.6. Like table 2.5, this table also shows real wages increasing in the early

United States often approximated zero in the 1930s, it is less clear that this

Depression, the same type of non-neutrality potentially affects nonfinancial

during the Depression.

Ben Bemanke is professor of economics and public affairs at Princeton University and a research

The authors thank

B)Why the U.S. Has Launched a New Financial World War -- and How the Rest of the World Will Fight Back

Michael Hudson is a former Wall Street economist. A Distinguished Research Professor at University of Missouri, Kansas City (UMKC), he is the author of many books, including Super Imperialism: The Economic Strategy of American Empire (new ed., Pluto Press, 2002) and Trade, Development and Foreign Debt: A History of Theories of Polarization v. Convergence in the World Economy . He can be reached via his website, mh@michael-hudson.com

2.3 The Link Between Deflation and Depression

Given the above discussion and evidence, it seems reasonable to accept theidea that the worldwide deflation of the early 1930s was the result of a monetary

contraction transmitted through the international gold standard. But this

raises the more difficult question of what precisely were the channels linking

deflation (falling prices) and depression (falling output). This section takes a

preliminary look at some suggested mechanisms. We first introduce here two

principal channels emphasized in recent research, then discuss the alternative

of induced financial crisis.

1.Real wages. If wages possess some degree of nominal rigidity, then falling

output prices will raise real wages and lower labor demand. Downward

stickiness of wages (or of other input costs) will also lower profitability, potentially

reducing investment. This channel is stressed by Eichengreen and Sachs

(see in particular their 1986 paper) and has also been emphasized by Newell

and Symons (1988).

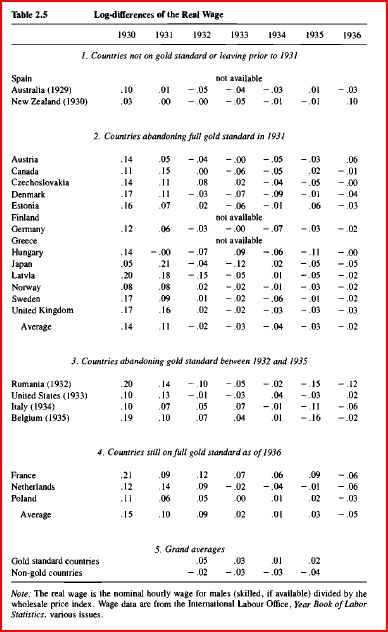

Some evidence on the behavior of real wages during the Depression is presented

in table 2.5, which is similar in format to tables 2.2-2.4. Note that

table 2.5 uses the wholesale price index (the most widely available price index)

as the wage deflator. According to this table, there were indeed large real

wage increases in most countries in 1930 and 1931. After 1931, countries

leaving the gold standard experienced a mild decline in real wages, while real

wages in gold standard countries exhibited a mild increase. These findings are

similar to those of Eichengreen and Sachs (1985).

The reliance on nominal wage stickiness to explain the real effects of the

deflation is consistent with the Keynesian tradition, but is nevertheless somewhat

troubling in this context. Given (i) the severity of the unemployment that

was experienced during that time; (ii) the relative absence of long-term contracts

and the weakness of unions; and (iii) the presumption that the general

public was aware that prices, and hence the cost of living, were falling, it is

hard to understand how nominal wages could have been so unresponsive.

Wages had fallen quickly in many countries in the contraction of 1921-22. In

the United States, nominal wages were maintained until the fall of 1931 (possibly

by an agreement among large corporations; see O'Brien 1989), but fell

sharply after that; in Germany, the government actually tried to depress wages

early in the Depression. Why then do we see these large real wage increases

in the data?

One possibility is measurement problems. There are a number of issues,

such as changes in skill and industrial composition, that make measuring the

cyclical movement in real wages difficult even today. Bernanke (1986) has

argued, in the U.S. context, that because of sharp reductions in workweeks

and the presence of hoarded labor, the measure real wage may have been a

poor measure of the marginal cost of labor.

Also in the category of measurement issues, Eichengreen and Hatton

(1987) correctly point out that nominal wages should be deflated by the relevant

product prices, not a general price index. Their table of product wage

indices (nominal wages relative to manufacturing prices) is reproduced for

1929-38 and for the five countries for which data are available as our table

2.6. Like table 2.5, this table also shows real wages increasing in the early

1930s, but overall the correlation of real wage increases and depression does

not appear particularly good. Note that Germany, which had probably the

worst unemployment problem of any major country, has almost no increase in

real wages; 10

the United Kingdom, which began to recover in 1932, has real

wages increasing on a fairly steady trend during its recovery period; and the

United States has only a small dip in real wages at the beginning of its recovery,

followed by more real wage growth. The case for nominal wage stickiness

as a transmission mechanism thus seems, at this point, somewhat mixed.

2.Real interest rates. In a standard IS-LM macro model, a monetary contraction

depresses output by shifting the LM curve leftwards, raising real interest

rates, and thus reducing spending. However, as Temin (1976) pointed

out in his original critique of Friedman and Schwartz, it is real rather than

nominal money balances that affect the LM curve; and since prices were falling

sharply, real money balances fell little or even rose during the contraction.

Even if real money balances are essentially unchanged, however, there is

another means by which deflation can raise ex ante real interest rates: Since

cash pays zero nominal interest, in equilibrium no asset can bear a nominal

interest rate that is lower than its liquidity and risk premia relative to cash.

Thus an expected deflation of 10% will impose a real rate of at least 10% on

the economy, even with perfectly flexible prices and wages. In an IS-LM diagram

drawn with the nominal interest rate on the vertical axis, an increase in

expected deflation amounts to a leftward shift of the IS curve.

Whether the deflation of the early 1930s was anticipated has been extensively

debated (although almost entirely in the United States context). We will

add here two points in favor of the view that the extent of the worldwide

deflation was less than fully anticipated.

First, there is the question of whether the nominal interest rate floor was in

fact binding in the deflating countries (as it should have been if this mechanism

was to operate). Although interest rates on government debt in the

United States often approximated zero in the 1930s, it is less clear that this

was true for other countries. The yield on French treasury bills, for example,

rose from a low of 0.75% in 1932 to 2.06% in 1933, 2.25% in 1934, and

3.38% in 1935; during 1933-35 the nominal yield on French treasury bills

exceeded that of British treasury bills by several hundred basis points on average."

Second, the view that deflation was largely anticipated must contend with

the fact that nominal returns on safe assets were very similar whether countries

abandoned or stayed on gold. If continuing deflation was anticipated in

the gold standard countries, while inflation was expected in countries leaving

gold, the similarity of nominal returns would have implied large expected

differences in real returns. Such differences are possible in equilibrium, if they

are counterbalanced by expected real exchange rate changes; nevertheless,

differences in expected real returns between countries on and off gold on the

order of 11-12% (the realized difference in returns between the two blocs in

1932) seem unlikely.12

3.Financial crisis. A third mechanism by which deflation can induce

depression, not considered in the recent literature, works through deflation's

effect on the operation of the financial system. The source of the nonneutrality

is simply that debt instruments (including deposits) are typically set

in money terms. Deflation thus weakens the financial positions of borrowers,

both nonfinancial firms and financial intermediaries.

Consider first the case of intermediaries (banks).13

Bank liabilities (primarily

deposits) are fixed almost entirely in nominal terms. On the asset side,

depending on the type of banking system (see below), banks hold either primarily

debt instruments or combinations of debt and equity. Ownership of

debt and equity is essentially equivalent to direct ownership of capital; in this

case, therefore, the bank's liabilities are nominal and its assets are real, so that

an unanticipated deflation begins to squeeze the bank's capital position immediately.

When only debt is held as an asset, the effect of deflation is for a

while neutral or mildly beneficial to the bank. However, when borrowers'

equity cushions are exhausted, the bank becomes the owner of its borrowers'

real assets, so eventually this type of bank will also be squeezed by deflation.

As pressure on the bank's capital grows, according to this argument, its

normal functioning will be impeded; for example, it may have to call in loans

or refuse new ones. Eventually, impending exhaustion of bank capital leads to

a depositors' run, which eliminates the bank or drastically curtails its operation.

The final result is usually a government takeover of the intermediation

process. For example, a common scenario during the Depression was for the

government to finance an acquisition of a failing bank by issuing its own debt;

this debt was held (directly or indirectly) by consumers, in lieu of (vanishing)

commercial bank deposits. Thus, effectively, government agencies became

part of the intermediation chain.14

Although the problems of the banks were perhaps the more dramatic in the

Depression, the same type of non-neutrality potentially affects nonfinancial

firms and other borrowers. The process of "debt deflation", that is, the increase

in the real value of nominal debt obligations brought about by falling

prices, erodes the net worth position of borrowers. A weakening financial

position affects the borrower's actions (e.g., the firm may try to conserve financial

capital by laying off workers or cutting back on investment) and also,

by worsening the agency problems in the borrower-lender relationship, impairs

access to new credit. Thus, as discussed in detail in Bernanke and Gertler

(1990), "financial distress" (such as that induced by debt deflation) can in

principle impose deadweight losses on an economy, even if firms do not

undergo liquidation.

Before trying to assess the quantitative impact of these and other channels

on output, we briefly discuss the international incidence of financial crisis

during the Depression.

Author: Ben Bemanke, Harold JamesConference Date: March 22-24,1990

Ben Bemanke is professor of economics and public affairs at Princeton University and a research

associate of the National Bureau of Economic Research. Harold James is assistant professor

of history at Princeton University.

The authors thank

David Fernandez, Mark Griffiths, and Holger Wolf for invaluable research

assistance. Support was provided by the National Bureau of Economic Research and the National

Science Foundation.

Notes

10. However, it must be mentioned that recent exponents of the real wage explanation

of German unemployment invoke it to account for high levels of unemployment

throughout the mid and late 1920s, and not just for the period after 1929 (Borchardt 1979).

11. In the French case, however, there may have been some fear of government

default, given the large deficits that were being run; conceivably, this could explain the

higher rate on French bills.

12. A possible response to this point is that fear of devaluation added a risk premium

to assets in gold standard countries. This point can be checked by looking at

forward rates for foreign exchange, available in Einzig (1937). The forward premia on

gold standard currencies are generally small, except immediately before devaluations.

In particular, the three-month premium on dollars versus the pound in 1932 had a

maximum value of about 4.5% (at an annual rate) during the first week of June, but for

most of the year was considerably less than that.

13. The effect of deflation on banks, and the relationship between deflation and

bank runs, has been analyzed in a theoretical model by Flood and Garber (1981).

14. An important issue, which we cannot resolve here, is whether government takeovers

of banks resulted in some restoration of intermediary services, or if, instead, the

government functioned primarily as a liquidation agent.B)Why the U.S. Has Launched a New Financial World War -- and How the Rest of the World Will Fight Back

For thousands of years tribute was extracted by conquering land and looting silver and gold, as in the sacking of Constantinople in 1204, or Incan Peru and Aztec Mexico three centuries later. But who needs a military war when the same objective can be won financially? Today’s preferred mode of warfare is financial. Victory in today’s monetary warfare promises to go to whatever economy’s banking system can create the most credit. Computer keyboards are today’s army appropriating the world’s resources.

The key to victory is to persuade foreign central banks to accept this electronic credit, bringing pressure to bear via the International Monetary Fund, meeting this last weekend. The aim is nothing as blatant as extracting overt tribute by military occupation. Who needs an army when you can obtain the usual objective (monetary wealth and asset appropriation) simply by financial means? All that is required is for central banks to accept dollar credit of depreciating international value in payment for local assets.

But the world has seen the Plaza Accord derail Japan’s economy by obliging its currency to appreciate while lowering interest rates by flooding its economy with enough credit to inflate a real estate bubble. The alternative to a new currency war “getting completely out of control,” the bank lobbyist suggested, is “to try and reach some broad understandings about where currencies should move.” However, IMF managing director Dominique Strauss-Kahn, was more realistic. “I’m not sure the mood is to have a new Plaza or Louvre accord,” he said at a press briefing. “We are in a different time today.” On the eve of the Washington IMF meetings he added: “The idea that there is an absolute need in a globalised world to work together may lose some steam.” (Alan Beattie Chris Giles and Michiyo Nakamoto, “Currency war fears dominate IMF talks,” Financial Times, October 9, 2010, and Alex Frangos, “Easy Money Churns Emerging Markets,” Wall Street Journal, October 8, 2010.)

Quite the contrary, he added: “We can understand that some element of capital controls [need to] be put in place.”

The great question in global finance today is thus how long other nations will continue to succumb as the cumulative costs rise into the financial stratosphere? The world is being forced to choose between financial anarchy and subordination to a new U.S. economic nationalism. This is what is prompting nations to create an alternative financial system altogether.

The global financial system already has seen one long and unsuccessful experiment in quantitative easing in Japan’s carry trade that sprouted in the wake of Japan’s financial bubble bursting after 1990. Bank of Japan liquidity enabled the banks to lend yen credit to arbitrageurs at a low interest rate to buy higher-yielding securities. Iceland, for example, was paying 15 per cent. So Japanese yen were converted into foreign currencies, pushing down its exchange rate.

It was Japan that refined the “carry trade” in its present-day form. After its financial and property bubble burst in 1990, the Bank of Japan sought to enable its banks to “earn their way out of negative equity” by supplying them with low-interest credit for them to lend out. Japan’s recession left little demand at home, so its banks developed the carry trade: lending at a low interest rate to arbitrageurs at home and abroad, to lend to countries offering the highest returns. Yen were borrowed to convert into dollars, euros, Icelandic kroner and Chinese renminbi to buy government bonds, private-sector bonds, stocks, currency options and other financial intermediation. This “carry trade” was capped by foreign arbitrage in bonds of countries such as Iceland, paying 15 per cent. Not much of this funding was used to finance new capital formation. It was purely financial in character – extractive, not productive.

By 2006 the United States and Europe were experiencing a Japan-style financial and real estate bubble. After it burst in 2008, they did what Japan’s banks did after 1990. Seeking to help U.S. banks work their way out of negative equity, the Federal Reserve flooded the economy with credit. The aim was to provide banks with more liquidity, in the hope that they would lend more to domestic borrowers. The economy would “borrow its way out of debt,” re-inflating asset prices real estate, stocks and bonds so as to deter home foreclosures and the ensuing wipeout of the collateral on bank balance sheets.

This is occurring today as U.S. liquidity spills over to foreign economies, increasing their exchange rates. Joseph Stiglitz recently explained that instead of helping the global recovery, the “flood of liquidity” from the Federal Reserve and the European Central Bank is causing “chaos” in foreign exchange markets. “The irony is that the Fed is creating all this liquidity with the hope that it will revive the American economy. … It’s doing nothing for the American economy, but it’s causing chaos over the rest of the world.” (Walter Brandimarte, “Fed, ECB throwing world into chaos: Stiglitz,” Reuters, Oct. 5, 2010, reporting on a talk by Prof. Stiglitz at Colombia University. )

Dirk Bezemer and Geoffrey Gardiner, in their paper “Quantitative Easing is Pushing on a String” , prepared for the Boeckler Conference, Berlin, October 29-30, 2010, make clear that “QE provides bank customers, not banks, with loanable funds. Central Banks can supply commercial banks with liquidity that facilitates interbank payments and payments by customers and banks to the government, but what banks lend is their own debt, not that of the central bank. Whether the funds are lent for useful purposes will depend, not on the adequacy of the supply of fund, but on whether the environment is encouraging to real investment.”

Quantitative easing subsidizes U.S. capital flight, pushing up non-dollar currency exchange rates

Federal Reserve Chairman Ben Bernanke’s quantitative easing may not have set out to disrupt the global trade and financial system or start a round of currency speculation that is forcing other countries to defend their economies by rejecting the dollar as a pariah currency. But that is the result of the Fed’s decision in 2008 to keep unpayably high debts from defaulting by re-inflating U.S. real estate and financial markets. The aim is to pull home ownership out of negative equity, rescuing the banking system’s balance sheets and thus saving the government from having to indulge in a Tarp II, which looks politically impossible given the mood of most Americans.

The announced objective is not materializing. The Fed’s new credit creation is not increasing bank loans to real estate, consumers or businesses. Banks are not lending – at home, that is. They are collecting on past loans. This is why the U.S. savings rate is jumping. The “saving” that is reported (up from zero to 3 per cent of GDP) is taking the form of paying down debt, not building up liquid funds on which to draw. Just as hoarding diverts revenue away from being spent on goods and services, so debt repayment shrinks spendable income.

So Bernanke created $2 trillion in new Federal Reserve credit. And now (October 2010) the Fed is proposing to increase the Fed’s money creation by another $1 trillion over the coming year. This is what has led gold prices to surge and investors to move out of weakening “paper currencies” since early September – and prompted other nations to protect their own economies accordingly.

It is hardly surprising that banks are not lending to an economy being shrunk by debt deflation. The entire quantitative easing has been sent abroad, mainly to the BRIC countries: Brazil, Russia, India and China. “Recent research at the International Monetary Fund has shown conclusively that G4 monetary easing has in the past transferred itself almost completely to the emerging economies … since 1995, the stance of monetary policy in Asia has been almost entirely determined by the monetary stance of the G4 – the US, eurozone, Japan and China – led by the Fed.” According to the IMF, “equity prices in Asia and Latin America generally rise when excess liquidity is transferred from the G4 to the emerging economies.”

Borrowing unprecedented amounts from U.S., Japanese and British banks to buy bonds, stocks and currencies in the BRIC and Third World countries is a self-feeding expansion. Speculative inflows into these countries are pushing up their currencies as well as their asset prices, but. Their central banks settle these transactions in dollars, whose value falls as measured in their own local currencies.

Michael Hudson is a former Wall Street economist. A Distinguished Research Professor at University of Missouri, Kansas City (UMKC), he is the author of many books, including Super Imperialism: The Economic Strategy of American Empire (new ed., Pluto Press, 2002) and Trade, Development and Foreign Debt: A History of Theories of Polarization v. Convergence in the World Economy . He can be reached via his website, mh@michael-hudson.com

(TO BE CONTINUED)

Labels: BOOKS

posted by The visioner @ 4:49 PM

![]()

![]()

0 Comments:

Post a Comment

<< Home